The self-reinforcing effect of market

The self-reinforcing effect of market

“The job of the entrepreneur isn’t to act prudently, to err on the side of caution. It’s to err on the side of reckless ambition. It is to take the risk that the market allows him to take.” - M. Lewis

Thank you, all 4500+ of you, for being part of the community! Stay tuned for new insights, upcoming community events, as well as various investment/ job opportunities.

And as always, please feel free to reach out via team@iterativeventure.com

**Note: this newsletter is not a prediction or investment advice but merely sharing our insights and learning.

Reflexivity

Lately, we’ve been dabbling into the theory of reflexivity, otherwise known as self-fulling prophecy, to look at the market from a macro point of view.

Reflexivity theory states that investors don't base their decisions on reality, but rather on their perceptions of reality instead. The actions that result from these perceptions have an impact on reality, or fundamentals, which then affects investors' perceptions and thus prices.

The process is self-reinforcing and tends toward disequilibrium, causing prices to become increasingly detached from reality.

Putting this into context, we had one of the longest-running bull markets from the late 2000s. In this period, the investor sentiment went from gloom, coming out of the Global Financial Crisis 07’ - 08’, to euphoria towards the 2020s with the help of government stimulus and credit easing.

So, what happens when there’s an extended period of a bull market? How does it end? One hypothesis is reaching a Minsky moment, an inflection point where asset values suddenly drop.

The long periods of bull markets encourage a diminished perception of overall market risk, which promotes highly-leveraged/ speculative investments, and as a result, it ends with an intense liquidity crisis when there’s a decline in underlying asset prices.

So how does reflexivity tie in with all of this and with now?

Due to the easy access to capital defining the last decade, companies and startups were able to more easily access liquidity allowing for better gains. This sets in motion for investors to invest ever more capital into both public and private markets, further reinforcing the gains.

The onset of COVID-19 disrupted the last rate hiking cycle from 2015-2020 when the Federal Reserve Board reset the Federal funds rate to near 0, causing further euphoria thus lengthening the aforementioned disequilibrium.

Reflexivity and Crypto

Combining this and with crypto’s alluring incentive of tokenizing/financializing everything, we see the compounded effect of risk-taking (pertaining to Michael Lewis’s quote) where we get ___-to-earn including taking steps (STEPN).

In essence, the market participants were in the game for speculative purposes more so than they were for bringing real adoption to crypto using the infrastructure for its intended purpose. That is to say, there was not a dearth of capital for crypto and other markets in general, but too much capital incentivizing speculative behavior and chasing return.

Resetting the cycle

Closing out the last chapter of bull run, we are relieved to see that there is a reversion to the mean and common sense where the real value is being asked for.

A couple of narratives in the space are gaining traction, including real-yield (sustainable business model) and bringing real-world assets to collateralize against cryptocurrencies.

Not to mention, there has been an increase in focus on building infrastructure for better privacy protection and scalability to enable mass adoption for both consumers and institutions alike.

Further read on reflexivity here.

Interesting bits from last week

Broad Market

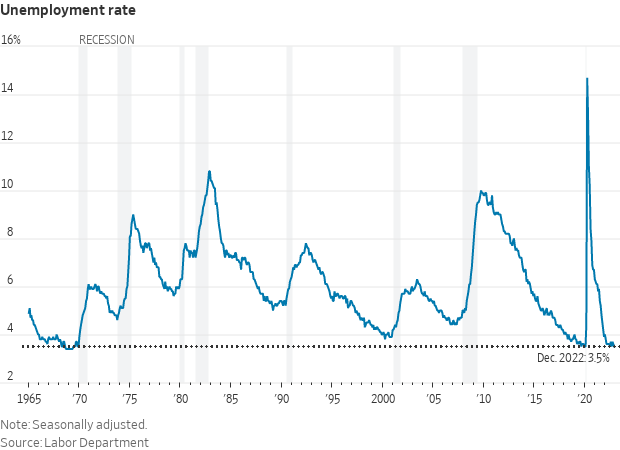

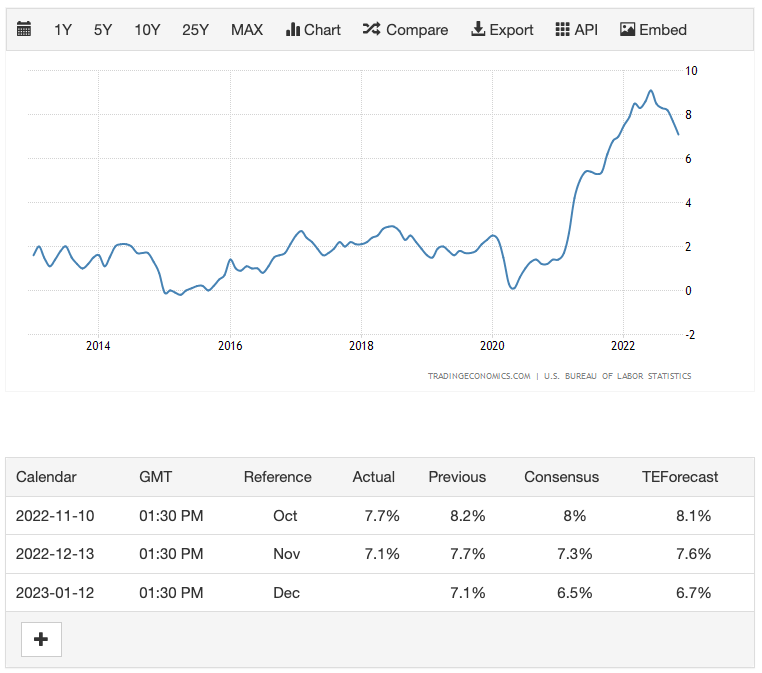

Jobs: There may be a reason to believe in a soft(-er) landing as the U.S. labor force participation went up while the unemployment rate came down. This is in addition to the easing inflation rate increase.

Labor Force Participation Rate Source

US Inflation Rate. Source

Venture Capital

The VC investment activities have slowed down significantly in 2H 2022, but it still remains higher than the pre-pandemic level.

And below are snippets of what happened with all these investments going into technologies:

Crypto

The number of crypto owners as of November 2022 crossed 400 million users, reaching approx. 5% of the global population

Developers are rushing in: 2022 saw the greatest influx of crypto builders as measured by Ethers.js and Web3.js package installs.

Last but not least - Bitcoin halving is coming up (approx. H1 2024), and if history serves as any indication, it may look upward again.

Partner Events

AllianceDAO, the leading Web3 founder community and accelerator, will be running its next cohort in Q1/Q2 2023. Alliance's reputation is well established as the premier community and DAO for founders, with a 1.8% acceptance rate. Accepted teams include 0x, Paraswap, Dodo, Apwine, Set, Ribbon, StepN, and many more.

You can learn more about Alliance in this presentation. The application deadline is on Jan 16th, 2023, and the cohort starts on March 2023.

Apply here.

We will come back with more interesting insights and community updates.

Happy Monday!